Option Types, "Moneyness"

and Intrinsic & Extrinsic Option Value

Types of Options:

Option Definition:

An Option gives the holder, the legal right, but not the obligation, to buy or sell an underlying asset eg a stock, currency or ETF, at a specific price by a specific time. They are a financial "derivative" because they derive their value from the underlying stock, currency or ETF that the contract refers to. Effectively you can use them to lock in a price agreed today (the Strike, K) for a future delivery.

That pricing relationship between the underlying and the option contract is determined by the Nobel Prize winning Black-Scholes-Merton Option Pricing formula that assumes a Normal (bell curve) Distribution of underlying prices around the mean or average.

It a nutshell, for relatively little outlay (buying to open) or renumeration (selling to open) -- you can obtain the price action in the underlying (at a Strike price agreed today) and potentially profit from eventual movements in that underlying.

Options are Classified into Two Types:

Call and Puts.

Each provides the holder specific rights to buy or sell an underlying asset at a predetermined price (the Strike price) before or on a specific date (the expiration date). You can buy or sell a Call or Put Option to open or close a position. Typically Options give you the right to obtain a specific number of units of the underlying asset. Eg Stock Options give you the right to obtain 100 shares of the stock at a price agreed today for future delivery. This is the length, in days remaining to expiry (DTE) of the contract. More below.

Both calls and puts can be used in complex strategies, hedging, or as standalone bets on market direction. Please refer to my Option Strategies page here.

Here's an overview of each type of Option:

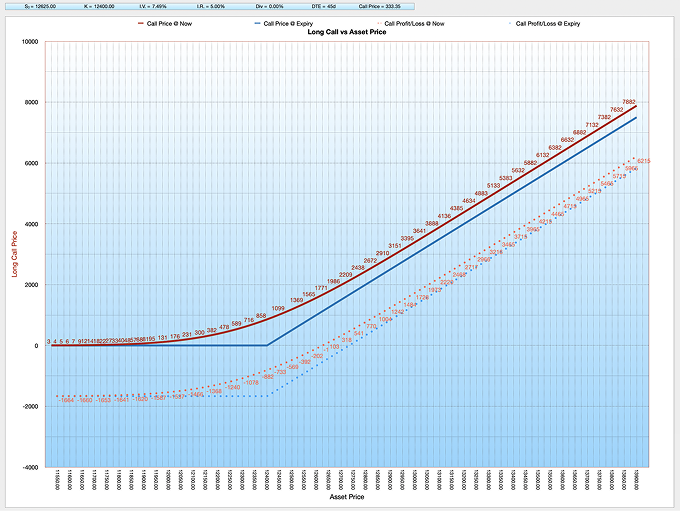

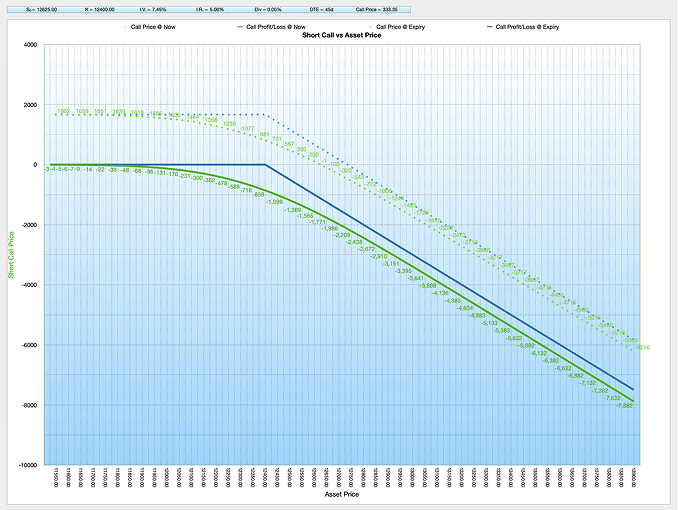

Long & Short Call Options:

A Call Option gives the buyer the right (but not the obligation) to buy the underlying asset at the strike price by the expiration date.

- Buyer Perspective: When you buy a Call, you expect the underlying asset's price to rise above the strike price by the expiration. You profit if the price exceeds the strike price plus the cost of the Call Option (the premium).

- Seller Perspective: Selling (or "writing") a Call obligates you to sell the underlying asset at the strike price if the buyer exercises the Option. Sellers of Calls hope the asset's price stays below the strike price so the Option expires worthless, allowing them to keep the premium.

- Example: Suppose a stock is trading at $100, and you buy a $105 Call for $3. If the stock price rises to $110 by expiration, you could exercise your Call and buy the stock at $105, then sell at $110, making a $5 gain. After accounting for the $3 premium, your profit is $2.

Long Call Option:

- Long Call Options are for buyers who are bullish (expecting the price to go up) on the asset.

Short Call Option:

- Short Call Options are for Sellers who are bearish (expecting the price to go down) on the asset.

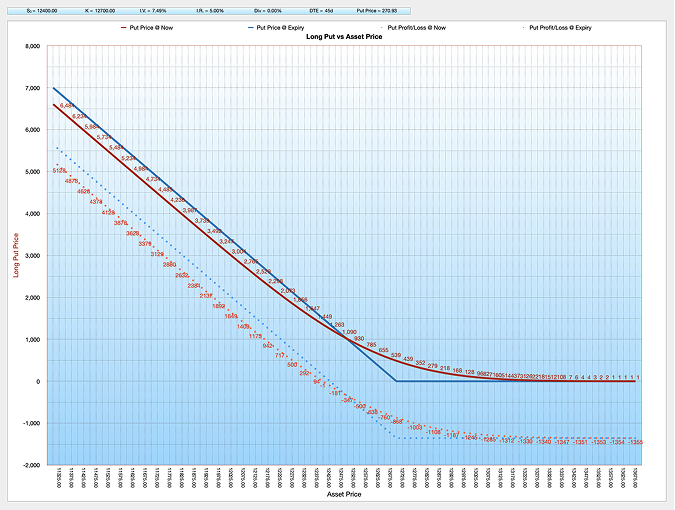

Long & Short Put Options:

A Put Option gives the buyer the right (but not the obligation) to sell the underlying asset at the Strike price by the expiration date.

- Buyer Perspective: When you buy a Put, you expect the underlying asset's price to drop below the strike price by expiration. You profit if the price falls enough to cover the cost of the Put Option (the premium).

- Seller Perspective: Selling a Put obligates you to buy the underlying asset at the strike price if the buyer exercises the Option. Sellers of Puts hope the asset's price stays above the strike price so the Option expires worthless, allowing them to keep the premium.

- Example: Suppose a stock is trading at $100, and you buy a $95 put for $3. If the stock price drops to $90 by expiration, you could exercise your put and sell the stock at $95, buying it at $90 in the open market, making a $5 gain. After accounting for the $3 premium, your profit is $2.

Long Put Option:

- Long Put Options are for buyers who are bearish (expecting the price to go down) on the asset.

Short Put Option:

- Short Put Options are for sellers who are bullish (expecting the price to go up) on the asset.

Option "Moneyness:"

In the Money (ITM) | At the Money (ATM) | Out the Money (OTM):

In Options trading, ITM, ATM, and OTM refer to the "moneyness" of an Option, which is a way to describe its current position relative to the underlying asset's price.

1. ITM (In the Money)

- Call Option: A Call option is in the money if the underlying asset's current price is above the option's strike price. This means the holder could buy the asset below its current market value.

- Put Option: A Put option is in the money if the underlying asset's current price is below the option's Strike price. This means the holder could sell the asset above its current market value.

Example: If a stock is trading at $100:

- A $90 Call Option is ITM because the holder can buy the stock at $90, below its market price.

- A $110 Put Option is ITM because the holder can sell the stock at $110, above its market price.

2. ATM (At the Money)

- An Option is at the money if the strike price is approximately equal to the current price of the underlying asset.

- For both Call and Put Options, being ATM means there is no intrinsic value because the strike price is right at the asset's market price.

Example: If a stock is trading at $100:

- A $100 Call or $100 Put is ATM.

ATM Options typically have the highest time value and are heavily influenced by volatility since their payoff potential is close to the underlying asset's current price.

3. OTM (Out of the Money)

- Call Option: A Call Option is out of the money if the current price of the underlying asset is below the Option's strike price. The holder would not exercise it because they could buy the asset cheaper at the market price.

- Put Option: A Put Option is out of the money if the underlying asset's price is above the Option's strike price. The holder wouldn't exercise it because they could sell the asset for more at the market price.

Example: If a stock is trading at $100:

- A $110 Call Option is OTM because buying at $110 is above the market price.

- A $90 Put Option is OTM because selling at $90 is below the market price.

OTM Options have no intrinsic value and consist purely of time value. They are often cheaper and used by traders expecting a significant move in the underlying asset.

Buying (to open) at Option that is Out the Money has a small chance of a large payoff. Selling (to open) at Option that is Out the Money has a large chance of a small payoff.

The probabilities and payoffs are derived from the Black-Scholes-Merton Pricing Model.

I remember reading about a trader that bought a $3,000 of Long Puts (that profit from a fall in the underlying prices) on the Dow Jones before the 1987 Stock Market Crash and turning that outlay into $1,000,000.

Option Mis-Pricing:

Important Note on Pricing of Long Dated Option Premiums:

Sometime around 2023, banks like the Union Bank of Switzerland and Saxo Bank (as examples I am aware of), started to manipulate the BSM Model pricing by using other metrics like "Order Flow," "Economic News flow" and other factors to price their longer dated quarterly options (3 months to contract expiry). Options are Over the Counter (OTC) securities that trade via a broker-dealer network instead of on a centralised exchange like the London Stock Exchange.

IG Index: May 2024:

"Please note that I have checked with our options desk and they have informed me our FX options are OTC products and these prices follow our own B&S model and we reflect the order flow that we receive. Therefore the B&S model that you might be following may differ to how we price our options on our platform.

More specifically the I.V. (Implied Volatility) that we are using may differ to the I.V. values you are using, please take this into account when you are trading options on our platform. The prices reflected are correct and I have confirmed this with the respective desk.

The factors that can also affect the pricing of our options are client sentiment, trading volumes that we receive and also market events such as CPI, Employment data and Interest rate announcements to name a few. As such, you would not be able to calculate the exact pricing of our Options (leveraged) based on your (BSM) calculator."

Well, for the last 50 years the Nobel Prize winning Black-Scholes-Merton Option Pricing Model was sufficient for banks and brokerage firms... Make sure you use an Option Price Calculator and know the true mathematical price of the Options you are buying or selling otherwise, for example, you could be shorting a long dated Cable (£/$) Call Option for a premium of $100 when the true mathematically derived price is eg $175... yes, I have seen pricing disparities this wide and up to 200 points of drift from the price the BSM would price the Option at for a certain Strike and the price offered by IG Index at the same Strike!

What does this mean?

It means you're more likely to have your Strikes challenged because when you add the premium to the Strike Price (K) you won't have as much distance or buffer (in the form of premium) between your Strike and underlying Price before it hits breakeven.

Eg: Trading a Short Call on the £/$ with a K = 12900 and Premium $100, you have until the Underlying Price (S) hits 13000 before your breakeven is reached. With the correct BSM derived premium of $175, you wouldn't need to adjust until the £/$ hits 13075 (assuming that Spot hitting your Strike is your adjustment/exit point).

The bank / broker is "conning you" and not adequately compensating you, via the premium you receive, for holding the short Option and carrying the risk that the underlying market price could breach your Strike Price (K).

Also remember the BSM assumes a Normal distribution of underlying prices and constant volatility but markets tend to have higher risks including large event risks, eg Covid.

Why has there been a Shift?

The risk shifted from the bank or broker to you. Banks don't like risk so push it to the client by adjusting their input parameters so the model produces premiums that favour them and protect against the risk that mispricing losses will come out of their pocket. That's why you need a Black Scholes Option Pricing Calculator on your desk, ideally on each monitor, showing you what the price should be at the Strike you want to trade at, so you know if you are being ripped off!

Note: The latest version of the 30x Banks BSM Option Pricer Calculator incorporates a new feature that alerts you with a visual notification of pricing drifts of over 25% and up to 150%+ or more from the Black Scholes Merton derived Option price. You can input the broker or bank's Option price and this is compared to the price given by the BSM formula. A drift from the BSM calculated price of more than 25% is alerted by a text notification that the broker or bank Option mispricing is occuring.

I haven't back tested the fact that there are major pricing discrepancies but I would imagine buying under priced Options and selling the over priced ones might be an area of investigation for these mis-priced long dated Options.

Intrinsic & Extrinsic Value:

Intrinsic Value of Options:

Intrinsic value is the actual, tangible value of an Option if it were exercised right now. It represents the difference between the Option's Strike Price (K) and the current Market Price of the Underlying Asset (S).

For Call Options, intrinsic value is calculated as:

- Intrinsic Value = Current Price of Asset - Strike Price.

A Call Option has intrinsic value if the asset's current price is above the Strike Price (K), meaning it's in the money (ITM). If the asset price is below the strike price, the intrinsic value is zero (it's out of the money, OTM).

For Put Options, intrinsic value is calculated as:

- Intrinsic Value = Strike Price - Current Price of Asset.

Key Points:

- Only ITM Options have intrinsic value; OTM Options have an intrinsic value of zero.

- Intrinsic value is distinct from time value (Theta), which is the additional amount in the Option's premium based on its potential to gain value before expiration.

Example:

If a stock is trading at $50, a $45 Call Option has an intrinsic value of $5, while a $55 Call Option has an intrinsic value of zero.

The intrinsic value helps in assessing the real, inherent worth of an Option, regardless of the remaining time until expiration or market volatility.

Extrinsic Value of Options:

Extrinsic value (also known as time value, Theta) is the portion of an Option's premium that exceeds its intrinsic value. It reflects the added value of the Option due to factors other than the difference between the underlying asset's price and the Option's Strike Price (K). Extrinsic value is influenced by time until expiration, volatility, and market conditions.

For Calls and Puts, the Extrinsic Value Formula is the same:

- Extrinsic Value = Option Premium − Intrinsic Value.

If an Option is out of the money (OTM), it has no intrinsic value, so its premium consists entirely of extrinsic value.

Extrinsic Value (Cont):

Factors Affecting Extrinsic Value:

- Time to Expiration: The longer the time left until an Option expires, the higher its extrinsic value. This is because there's more time for the underlying asset's price to move in favour of the Option. As expiration approaches, the extrinsic value decreases, a phenomenon known as time decay (measured by the Greek "Theta").

- Volatility: Higher volatility increases extrinsic value, as it raises the chance of the Option becoming profitable. Options on assets with higher volatility are typically more expensive due to this added uncertainty (measured by the Greek "Vega").

- Interest Rates and Dividends: Changes in interest rates and expected dividends can slightly impact extrinsic value, though this effect is generally minor compared to time and volatility.

Suppose a stock is trading at $50:

- A $45 Call Option, which is in the money, has a premium of $7. If its intrinsic value is $5 (current stock price - strike price), then its extrinsic value is $2.

- A $55 Call Option, which is out of the money, has no intrinsic value. If its premium is $1.50 then the entire $1.50 is extrinsic value.

Key Points:

- Only Options with time remaining until expiration have extrinsic value.

- Extrinsic value declines over time as expiration nears, a process called time decay (Theta).

- Extrinsic value can be higher in volatile markets as there's a greater possibility of the Option becoming profitable.

In summary, extrinsic value reflects the market's perception of an Option's potential value due to time and volatility, beyond its intrinsic value.

Why does the Live @Now Long Put Option price dip below the @Expiry Price?

There are a number of factors that cause this. Please refer to my Option Interest Rates page here.